by L Carlos Lara

There are many reasons for believing that a dividend-paying whole life insurance policy from a mutual insurance company is one of the last remaining bastions of safety and growth for our savings here in the United States. This unequivocal standard of financial supremacy is highlighted when considering the state of our economy, the constant encroachments of government into our private lives, and the Federal Reserve’s loose monetary policy. Those of us who are privileged to own one or more of these policies are well aware of their multi-dimensional tax-free benefits, the reasonable measure of guarantees which they offer, and the unencumbered access to our money when it is needed. If death should occur in the midst of our efforts to save our money inside of these policies, the entire savings plan immediately self completes and our beneficiaries are endowed with an estate that would otherwise take a lifetime to build.

Additionally, their most exceptional, but often overlooked attribute is that as policyholders we are also owners of the mutual insurance company. No other financial instrument offered by any institution offers such an array of benefits to individuals and businesses. This is because mutual life insurance companies are organizations that are owned and controlled by patron members. As owners of mutual life insurance companies, not only are we individually rewarded with the residual earnings of the company, but collectively we also represent one of the most formidable sources of investment for strengthening our economy. One wonders why present-day Americans are so ill informed about these invaluable marks of distinction and why there is so much confusion surrounding dividend-paying Whole Life.

This article is intended to provide a clue to these questions as well as to reinforce upon the financial advisor the importance of sound economic education as he talks to his clients about this very important financial instrument and the industry that provides it.

What is a Cooperative?

We should begin our query by examining the definition of a cooperative. Upon inspection of this term the mind’s eye immediately evokes an entire series of characteristics that can be summed up in the words “user owned—user controlled businesses.” However, trying to find out more in-depth facts about cooperatives is difficult. In fact, very little is actually known about this unique sector and the impact they actually have on our economy. For example, none of the business reporting agencies of the U.S. government directly provides or tracks such information; consequently independent studies are our only real source of verifiable data on cooperatives and this information is scarce.

One of the most reliable independent studies to be done in recent years (revised June 19, 2009) is the report provided by the University of Wisconsin Center for Cooperatives. This project was funded by the U.S. Department of Agriculture with matching support from the National Cooperative Business Association. In this in-depth report we learn some remarkable facts about cooperatives:

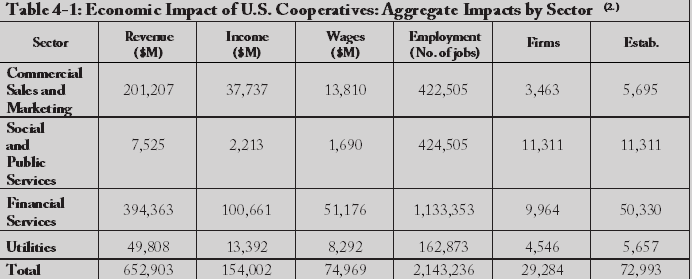

There are nearly 30,000 U.S. cooperatives operating at 73,000 places of business throughout the United States. These cooperatives own $3 Trillion in assets, and generate $500 Billion in revenue and $25 Billion in wages. Extrapolating from the sample to the entire population, the study estimates that cooperatives account for nearly $654 Billion in revenue, 2 Million jobs, $75 Billion in wages and benefits paid, and a total of $133.5 Billion in value-added income.

Americans hold 350 Million memberships in cooperatives, which generate nearly $79 Billion in total impact from patronage refunds and dividends. Nearly 340 Million of these memberships are in consumer cooperatives. (1.)

There are four major aggregate economic sectors where cooperatives are active.

1. Commercial Sales and Marketing: Farm supply and marketing; Biofuels; Grocery and Consumer Retail Goods; Arts and Crafts and Entertainment.

2. Social and Public Services: Housing; Healthcare; Daycare; Transportation; Education

3. Financial Services: Credit Unions; Farm Credit; and Mutual Insurance

4. Utilities: Electric; Telephone; Water

Ownership Considerations

Aside from the impressive aggregate impact on the economy by sector as reflected in Table 4-1, we should also be aware that cooperatives are fundamentally different from other forms of business.

Traditionally, the defining characteristics of a cooperative business are that the interests of the capital investor are subordinate to those of the business user, or patron, and returns on capital are limited. Cooperative control is in the hands of its member-patrons, who democratically elect the board of directors. Member-patrons are the primary source of equity capital, and net earnings are allocated on the basis of patronage instead of investment. (3.)

In other words, patron ownership is a defining characteristic. Ownership is characterized by control rights and rights to residual returns.

The University of Wisconsin study used five potential qualifying criteria in order to determine whether or not a given firm is a cooperative. These five criteria include: (1.) A Statement of Principles, (2.) Self- Identification, (3.) Incorporation Status, (4.) Tax Filing Status, and (5.) Governance Structure.

There was considerable ambiguity found from the data collected from (2.) Self-Identification and (3.) Incorporation Status. In the case of Self-Identification, the study found that some organizations use the term “cooperative” only descriptively to mean a functional approach that includes collaboration among its members, but are neither owned nor controlled by patron members.

With regards to Incorporation Status, this criterion also lacked a definitive indicator to provide a comprehensive cooperative census. This was due in part to the fact that incorporation is done at state levels and state statutes are not uniform. Furthermore, under some state statutes, cooperatives are considered a type of nonprofit corporation. General nonprofit statutes permit member organizations, but may not guarantee the right of members to vote. General nonprofit statutes also prohibit distributing residual earnings to those who control the organization, including members.

Despite these ambiguities, tax-filing status, or more specifically, federal tax code filing requirements are consistent across all states and reflect how a particular entity operates. This provided a quantifiable indicator of an entity’s cooperative character.

Federal tax law recognizes that cooperatives provide patron benefits instead of profits to investors, and that their residual earnings are passed through to patrons. These earnings typically are taxed once, at the patron level. The cooperative files its tax returns using a cooperative version of the corporate income tax return to qualify for the single taxation treatment. In these cases, the type of tax form submitted clearly identifies the organization as a cooperative.

Federal tax code also grants tax exemptions to certain cooperatives operating in specific sectors, treating them as not-for-profit entities. Mutual utilities, credit unions, mutual insurance companies, farm credit organizations, and some farmer cooperatives are examples of cooperative sectors that receive Federal tax-exempt designations. These cooperatives file for tax exemptions on earnings using the same standard nonprofit tax form as other nonprofit and non- cooperative organizations. It is this tax-exempt status that identifies these organizations as cooperatives.(4.)

Moreover, eighty-five percent (85%) of all U.S. revenue from cooperatives is determined from incorporation status and tax filings generated within seven sectors:

- Agriculture,

- The Farm Credit System

- Federal Home Loan Banks

- Rural Electric Service

- Mutual Insurers

- Credit Unions.

Unlike other scarce statistics about cooperatives, this particular information is readily available from government or trade associations. Consequently, when used in combination, an organization’s incorporation status and its tax filing, or tax-exempt status, can be used to clearly identify cooperatives.

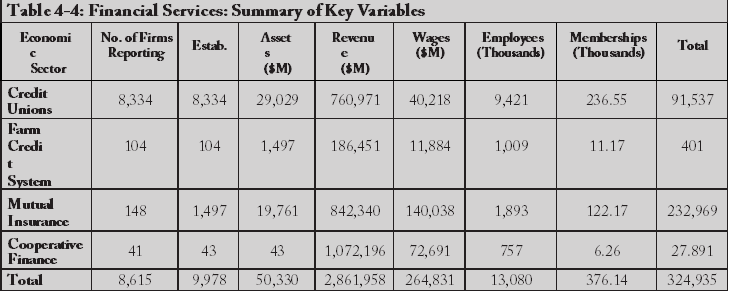

Financial Services

Financial Services are the largest aggregate sector of all cooperatives in the United States. This sector includes Credit Unions, the Farm Credit System, Mutual Insurers, and a small number of very large financial institutions that provide loan funds to cooperative businesses (or that operate on a cooperative basis with member businesses). Credit Unions and Mutual Insurance companies account for the largest number of firms, establishments, members, and employees.

Table 4-4 above shows that 8,615 of the 50,330 financial service cooperatives in the U.S. provided information for the Wisconsin Report. These “reporting” cooperatives account for $2.8T in assets, $265B in revenue, 376,000 jobs and $13B in wages. There are a total of 325 million members in the financial services sector of cooperatives.(5.)

The Mutual Insurance Company

The Wisconsin Report further indicated that the global industry of insurance collects $4 trillion in premiums annually. In the United States alone there are 2,723 property casualty insurance companies with $1.3 trillion in cash and invested assets. The cash and invested assets of the 1,190 Life and Health insurance companies was more than twice that amount, at $3 trillion. Of course most of these entities are not identified as cooperatives and as banking and insurance services have merged within the financial sector, many of these companies are part of larger entities.

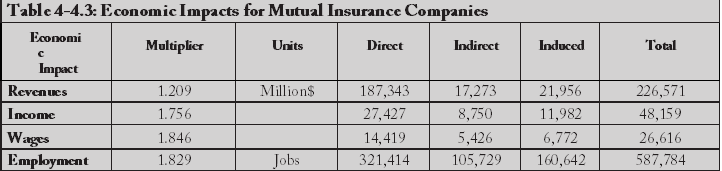

Table 4-4.3 below summarizes the data for the Mutual Insurance sector specifically and shows that at the time of the study, mutual insurers accounted for $227 billion in revenue, 500,000 jobs, $27 billion in wages paid, and $48 billion in valued-added income.(6.)

Background

The first mutual insurance company was formed in England over three hundred years ago (1696). Farmers began the mutual insurance industry by first creating informal associations within their local communities to deal with the catastrophic loss of fire. By spreading the risk amongst a large pool of participants the rates required to cover for this loss became readily affordable. By 1870 legislation formalized their existence and the industry flourished nationwide in England.

According to the Wisconsin Report, the life insurance industry was almost nonexistent in the United States before the advent of the mutual model. “Benjamin Franklin founded the American Mutual Property and Casualty Insurance Industry in 1752 when he established the Philadelphia Contributionship.”(7.) The first mutual insurance companies were created in 1843, and the number grew to 19 by 1849. Mutual ownership companies became the fastest growing models for life insurance companies in the United States until 1859 when the viability of stockholder-owned firms came into vogue.

Structure

As the Wisconsin report explains, the interest in a mutual insurance company by its policyholders comes in two forms. Policyholders are holders of an insurance policy that defines a set of rights, and they are also holders of a set of ownership interests. When an individual purchases a policy his ownership in the company begins and it ends with the termination of the policy. This is in stark contrast to a situation where ownership derives from purchase of a share of stock, and that ownership can continue during periods of use or non-use of an insurance policy from the stock company.

In a mutual insurance company ownership interests include governance and economic participation in the firm. Owners of policies have the right to vote for the board of directors. In most states, policyholders have rights to the distribution of the assets upon dissolution of the company. Although the individual policy owner does not directly have the right to decide on the use of company profits, he is nevertheless aware that they can only go into two places— they can be added to the surplus of the company, or distributed to members in the form of policy dividends. In stock-owned insurance companies, owners can potentially gain from changing the firm’s dividend distribution after insurance contracts are sold. In mutually owned firms—the kind that Nelson Nash recommends to his readers—policyholders and owners are merged, eliminating the potential conflict over what to do with profits, as exists in a stockholder-owned insurer.

Demutualization

While the organizational structure of a mutual insurance company certainly appears to have superior benefits over stock companies as far as policyholders are concerned, the Wisconsin Report alludes to a heightened opportunity for conflict between management and policyholders—the owners of the company. Interviews with management in mutual insurance companies reveal that many of the devices used in stock-owned firms are simply unavailable to them (e.g., access to capital, stock takeovers, monitoring by stock analysts, and stock-based compensation programs). With a traditional stock company—even if we set aside insurance for the moment—if the managers aren’t doing a good job maximizing shareholder value, then the company’s net assets are worth more than its book value, and it becomes a ripe target for a “hostile takeover.” This process is vilified in the popular media (in movies such as Other People’s Money starring Danny DeVito) but it actually protects the distant shareholders from having the day-to-day managers effectively drain the resources out of a company to their own benefit.

The potential problem, as the Wisconsin Report emphasizes, is that this circuit-breaker mechanism is unavailable to a mutual insurance company. Here, if the management isn’t acting in the best interests of the owners (i.e. the policyholders), it’s hard for an outsider to come in and clean house, because he or she would have to go around to policyholders and buy them out. This is much more cumbersome than making a buyout offer to owners of stock.

For these reasons, it is crucial that the policyholders in a mutual life insurance company are educated about the nature of the instrument and its special niche in our economy. Ill-informed investors can get by owning shares of stock in corporations about which they know very little, because if things got really bad, a third-party takeover specialist would have the incentive to come in and fix it. Yet there is no savior at hand for a mutual insurer that is poorly run, for the reasons discussed above. It is up to the current owners to make sure the company is run properly, and the owners in a mutual company are the policyholders themselves.

If we have concluded that it is the responsibility—indeed the duty—of the policyholders to make sure the mutual insurance model survives in our volatile economic environment, this raises the obvious question: Who will educate the policyholders? The answer, of course, is the agents who originally sell them their policies.

In the past, the career agents were the sole disseminators of all the unique characteristics of the mutual insurance industry and they were adequately trained to pass on this valuable information to the buying public. Today, all of this has changed. Insurance carriers now rely heavily on independents to sell their products and unfortunately many of them are ill-trained and inexperienced.

Furthermore, the insurance industry underwent significant structural changes in the past 20 years, particularly after the passage of legislation in the 1990s that removed some barriers between insurance companies and banks. A significant number of mutual companies wanted to diversify their activities beyond insurance products as the stock market emerged into prominence. This new direction involved a greater need to access capital in order to grow, and consequently many mutual companies demutualized in the 1990s. Some converted completely to stock ownership. Others formed mutual holding companies that are owned by the policyholders of a converted mutual insurance firm. The holding companies can own one or more stockholder-owned insurance firms, and have the opportunity to own banking subsidiaries.

These dramatic changes within the industry have changed the mutual life insurance landscape. Today, the universe of mutual life insurance companies has been greatly reduced. Recent research indicates only 39 mutual life insurance companies remaining in the United States.

Conclusion

The cooperative ownership model is used extensively in the United States, ranging from the production and distribution of farm products to energy and home health care services to the elderly. Although cooperative businesses are responsible for a sizable positive impact on our overall economy, very little is actually known about them. Of all of the various economic sectors of cooperative businesses in the United States, financial services comprise the largest segment and the mutual insurance industry has the most members.

As the state of our economy worsens, savers and investors alike are looking for new sources of safety and return for their money, but for the most part are completely ignorant of the benefits found in mutual ownership. For those of us who have discovered the benefits that come from the idea of owning a piece of the company as opposed to the idea of being a source of profits for investors, the feelings are akin to being in possession of the best kept secret in money and finance.

Unfortunately, mutual life insurance companies that sell the preeminent dividend-paying whole life product are in the decline. This fact alone should cause all of us to think soberly about the state of our industry and do all that we can to help reverse this trend. All who are connected to the mutual life insurance industry, as management, agent, or policyholder, must recognize their responsibility as part of a cooperative effort to help each other, our businesses and our economy.

Sound economic education and the dissemination of it to the general public is the necessary catalyst for this turnaround. The Lara-Murphy Report is fully dedicated to this effort. In the small but crucial niche of mutual insurance companies, we must educate ourselves if we wish to continue implementing the amazing strategies that Nelson Nash and his followers have discovered. Within a cooperative business, no outsider has the incentive to swoop in and rescue us from our own bad judgment. It’s up to us.

Cooperatives Bibliography

1. Research on the Economic Impact of Cooperatives, Deller, Hoyt, Hueth, and Sundaram-Stukel, University of Wisconsin Center for Cooperatives, Revised June 19, 2009, Page 2

2. Research on the Economic Impact of Cooperatives, Page 15

3. Research on the Economic Impact of Cooperatives, Page 4

4. Research on the Economic Impact of Cooperatives, Page 5

5. Research on the Economic Impact of Cooperatives, Page 38

6. Research on the Economic Impact of Cooperatives, Page 44

7. The Philadelphia Contributionship, Company History, http://www.contributionship.com/history/index.html, February 26, 2012, 3:50 pm ct